Over the past few years, one expression has become common across banks: Basel IV.

It is heard in ALM committees, risk departments and discussions between finance teams and business lines. Yet officially, this term does not exist. Regulators continue to refer to the “finalisation of Basel III”. This distinction is not merely semantic — it reflects the very philosophy of the reform.

In reality, Basel IV is not a new regulatory framework. It is a strengthened, refined and more harmonised version of Basel III. The objective remains unchanged: to reinforce the resilience of the banking system after the 2008 financial crisis. However, years of implementation have revealed a key issue — comparable banks could report significantly different capital levels depending on their internal models. The recent adjustments aim primarily to reduce these discrepancies.

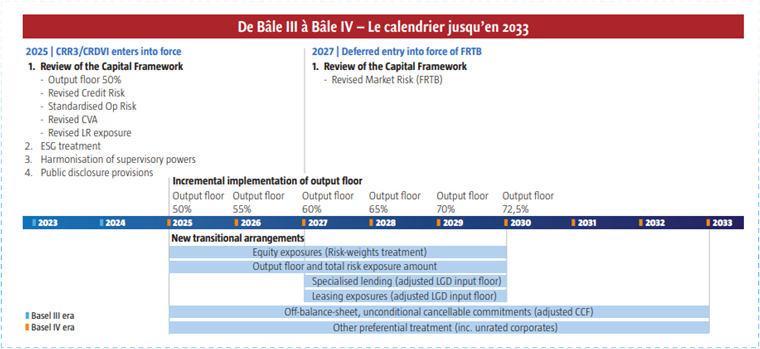

At the core of the reform lies the output floor. Its principle is straightforward: risk-weighted assets calculated using internal models cannot fall below 72.5% of those calculated under standardised approaches.

Sophistication is still allowed, but it can no longer endlessly reduce capital consumption.

This represents a major shift in logic. For years, the ability to develop advanced internal models was a competitive advantage. That advantage is now framed within clear boundaries. Models are not disappearing, but they are being brought back into a common corridor.

This is one of the main reasons why banks have adopted the term Basel IV: the philosophy has changed. The industry is moving from a system where optimisation played a central role to a more harmonised and comparable framework.

But this is not the only evolution.

Credit risk has been significantly revised. The scope of internal models has been restricted, and key parameters are now subject to floors. Standardised approaches have become more risk-sensitive, particularly for real estate exposures, specialised lending and off-balance-sheet commitments.

The objective is clear: to prevent structural underestimation of risk.

Operational risk is also evolving. Former methodologies — often complex and highly dependent on internal modelling — are being replaced by a simpler, standardised approach. Once again, the guiding principles are comparability and readability.

Counterparty risk and market risk are also being reshaped. The Fundamental Review of the Trading Book (FRTB), postponed to 2027 in Europe, redefines the boundary between the banking book and the trading book while strengthening sensitivity to market conditions.

Taken individually, these adjustments may appear technical. Taken together, they produce a structural effect: a reduction in banks’ room for interpretation when calculating capital requirements.

Yet the most silent transformation may lie elsewhere — in data.

The reform goes beyond capital ratios. It deeply reshapes prudential reporting and external disclosure. Data reported to supervisors and data published under Pillar 3 are now converging.

Every prudential figure becomes potentially public. This increase in transparency raises the bar significantly in terms of data quality, consistency and traceability.

Banks must now produce two views of capital: one based on internal models and another incorporating the prudential floor.

This dual perspective changes internal steering. An activity that appeared efficient under historical modelling assumptions may become more capital-consuming once the floor applies.

This shift explains why the term Basel IV has gained traction. It may not represent an official regulatory break, but it clearly reflects an operational one.

Why, then, do supervisors avoid this term?

Because they want to emphasise continuity. From their perspective, this is not a new philosophy but the logical completion of the post-crisis framework. Acknowledging a Basel IV would imply that Basel III was incomplete.

Why, on the other hand, do banks continue to use it?

Because it helps describe an internal change of paradigm. Capital steering becomes more constrained, more standardised and increasingly data-driven. The impact on pricing, capital allocation and commercial strategy is significant enough to justify a new label in everyday language.

In practice, the truth lies somewhere in between.

Yes, Basel IV does not exist legally.

Yes, it is the final stage of Basel III.

But yes as well: for banks, the transformation is deep enough to feel like a new chapter.

The gradual implementation through 2033 confirms that this is not a simple technical update.

It is a long adaptation phase requiring changes in organisations, systems and management culture.

Ultimately, the real novelty is not regulatory — it is managerial.

Capital becomes a resource to be actively managed in real time, just like liquidity or commercial profitability. Business decisions will increasingly need to integrate prudential considerations from the outset.

Perhaps that is the best definition of what the market calls Basel IV: not a new standard, but a Basel III that has reached maturity.

And as often in banking, what changes most is not the rulebook itself — but the way institutions learn to live with it.

Benoit Frayer